Texas has always had a large industrial base, but the data center boom of the past few years has transformed the state's load profile. Today, ERCOT sits on a bigger stack of flexible, controllable load than it has ever had. Load Resources (LRs), including Controllable Load Resources (CLRs) and Non-Controllable Load Resources (NCLRs), are drawing renewed interest as operators look for smarter ways to leverage flexibility.

Three trends are converging to accelerate that growth: falling ERS prices, regulatory changes that are lowering the barriers to market participation, and a new generation of technology that enables sophisticated market participation. Together, they point toward a future where flexible loads participate not through out-of-market programs like ERS, but directly in ERCOT's Energy and Ancillary Services (A/S) wholesale markets.

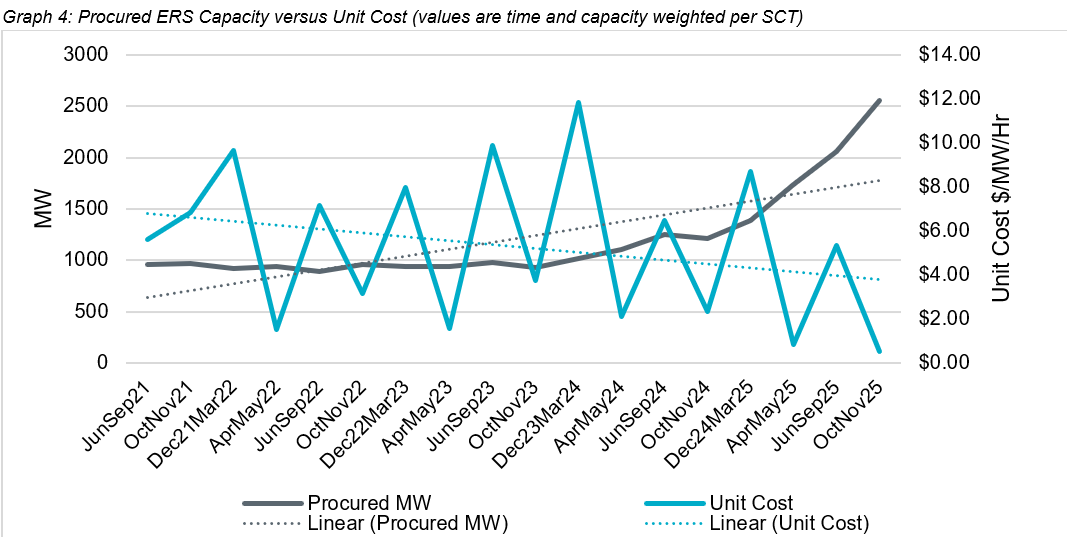

1. ERS prices are falling

The Emergency Response Service (ERS) program was originally designed for non-price-sensitive commercial and industrial loads: customers willing to curtail on short notice in exchange for a capacity payment. Over time, though, more price-sensitive and 4CP-sensitive loads found their way into the program. Participation grew and, as more megawatts competed for ERS contracts, prices fell. Payments that once made program participation worthwhile are no longer as attractive to legacy participants.

Source: ERCOT 2025 Annual Report on Demand Response in the ERCOT Region, January 30, 2026

2. The barriers to entry are coming down

Load Resources offer direct participation in ERCOT's Energy and A/S markets, and CLRs in particular are attractive because they gain access to nodal pricing. But historically, wholesale participation carried enough operational and regulatory complexity to deter all but the most sophisticated operators.

That's changing. Two pending rule changes, NPRR1244 and NOGRR263 (both taking effect in January 2027), remove the requirement to provide Primary Frequency Response (PFR). The practical effect is that loads that previously couldn't qualify for wholesale participation will be able to after January 2027. That's a direct expansion of the addressable market.

3. Technology is making participation operationally feasible

Operational controls and automation

Regulatory clarity helps, but it doesn't solve the operational challenge of actually running a Load Resource in ERCOT's wholesale markets. That has historically required specialized controls, telemetry infrastructure, and round-the-clock operational processes. Facilities needed to reliably respond to ERCOT dispatch signals, manage telemetry requirements, and stay in compliance with performance standards. These are demands that most industrial operators simply aren't set up to handle in-house.

On the controls side, a new generation of vendors has made automated dispatch genuinely accessible. Companies like OBM now offer control systems that allow facilities to respond to ERCOT dispatch instructions without manual intervention. The operational burden drops significantly, and reliability improves.

Forecasting and market participation

Operational controls solve the "how do we respond when dispatched" problem, but LR participation also requires daily decisions about when and how much capacity to offer into the market. Those decisions depend on a constantly shifting mix of variables: power prices, weather, grid conditions, reserve deployments, and market risk.

For some loads (crypto miners being the clearest example) the optimization problem is even more complex. Load strike prices change daily based on mining profitability and bitcoin prices, which means bid curves need to reflect both power market conditions and underlying business economics. Historically, a human had to update those curves before the QSE submitted them into the market each day. That's not scalable.

Today, forecasting and optimization platforms can automate much of this process. By forecasting prices, reserve deployments, weather, and grid conditions, operators can make more informed participation decisions and dynamically adjust market offers as conditions change, without a human in the loop for every update.

Load Resources are starting to look like batteries

As LR participation becomes more sophisticated, the operational problem increasingly resembles battery optimization. Both require price forecasting, bid optimization, automated dispatch, active market operations, and settlement and performance management.

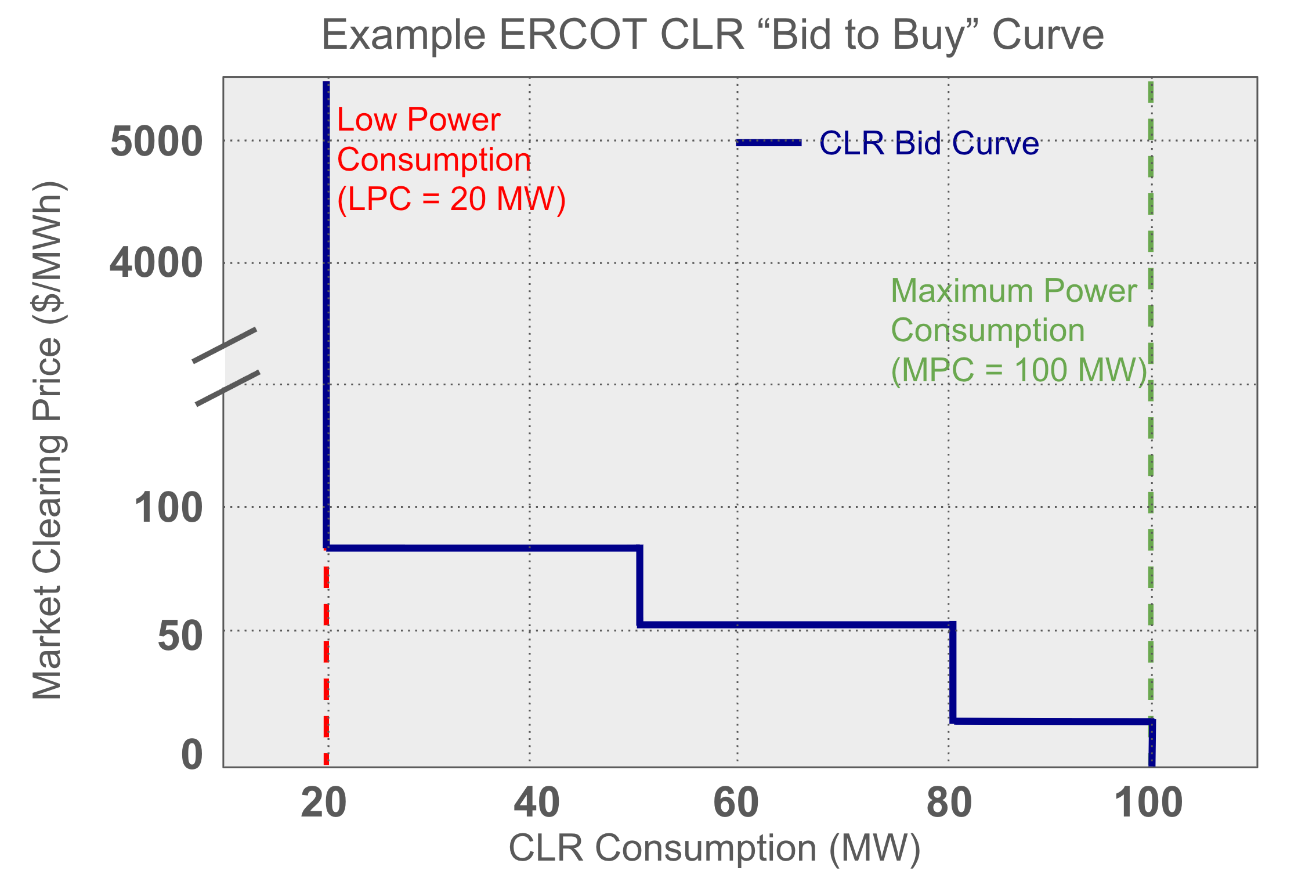

To see why, consider how a CLR actually participates in the ERCOT market. As shown above, a facility with 100 MW of total load might designate 20 MW as critical load (always online regardless of price) and 80 MW as flexible load that responds automatically to market prices. That creates a "bid to buy" curve the facility submits into ERCOT: at high prices, it curtails flexible load; at low prices, it consumes more. The bid curve can be customized based on the facility's specific economics, and it changes as market conditions change. That's not so different from how a battery operator decides when to charge and discharge.

What we've learned operating flexible resources

Gridmatic optimizes grid-scale batteries in both CAISO and ERCOT, with results that speak for themselves: we operate the #1-ranked 2-hour battery in ERCOT (2025) by TB2 uplift, and the #1-ranked battery in CAISO (2024–2025), and we're approaching 2 GWh of contracted storage in CAISO and ERCOT. That track record is built on the same core capabilities that Load Resource participation demands: best-in-class price forecasting, automated bid optimization, and market operations that run 24/7 without manual intervention. The same forecasting and optimization infrastructure that maximizes battery revenues can be applied directly to flexible load.

The opportunity ahead

Wholesale market participation is an increasingly attractive opportunity for flexible loads. ERCOT is actively lowering the barriers to CLR participation. And the technology to operate a Load Resource with the sophistication that good market participation requires now exists and is accessible.

Operators that can accurately forecast prices, optimize their bids, and automate their market participation will be positioned to capture significantly more value from the flexibility they already have. The window to build those capabilities, or find partners who have them, is opening.